Featured

Table of Contents

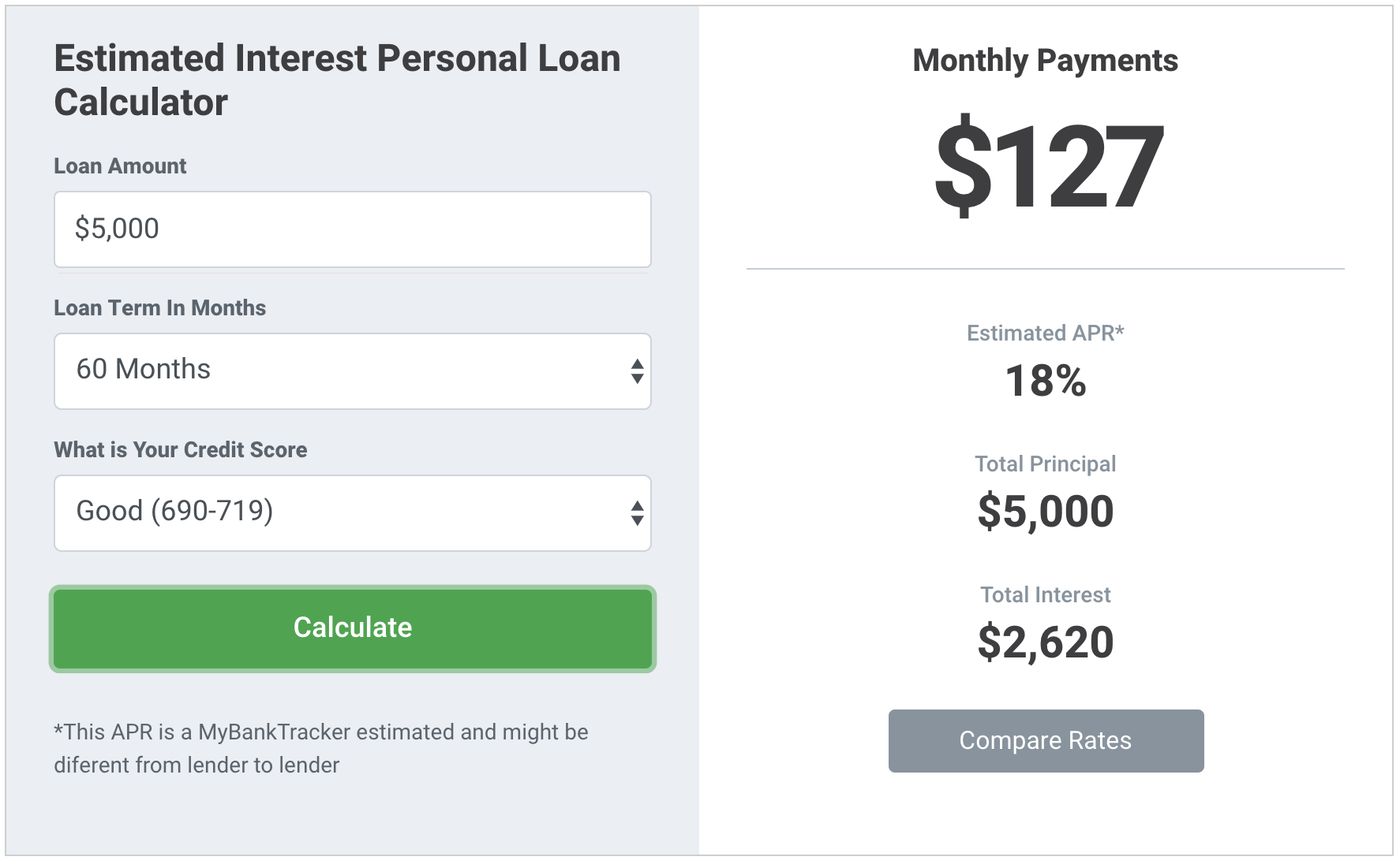

Customize your loan with amounts from $3,000 to $100,000 and terms from 12 to 84 months.

When you register with Experian, you can see the loan offers that are matched to your credit profile. Some individuals call these "soft pull loans"; they are individualized loan offers matched to your credit profile that you are most likely to be authorized for. Examining rates and your pre-qualified choices generates a soft inquiry, which will not harm your credit report if you aren't approved.

If you aren't at first authorized, the application will stay as a soft query. Approval is not ensured with the initial application, as there might be additional confirmations needed from the lender. If you are authorized for the deal, a tough query will be reported, along with the brand-new account, which might impact your credit history.

Ways to Consolidate Credit Debt

Signing up or logging in to view the loan uses matched to your credit profile will not affect your credit rating. When you use, choosing a loan labeled No Ding Decline will generate a soft inquiry if you aren't authorized and won't impact your credit history. Generally, requesting a loan, even if you aren't authorized, creates a tough query.

While that effect is generally very little and momentary, a single hard questions will typically take fewer than five points off your FICO Score, with this score effect staying for approximately a year. If you are authorized, a hard query will appear on your credit report, together with the new loan account, which might affect your credit scores.

Your credit scores ought to rebound within a few months, when you show your finances are stable with on-time payments. Ultimately, your credit history might likewise improve as your on-time payment history continues with responsible management of your new financial obligation.

Modern Debt Solutions for Tulsa Credit Card Debt Consolidation WorkersDiscover the Finest Personal Loans U.S.A. 2026. Compare leading lenders, APR rates, approval tips, charges, and expert strategies to borrow securely with low interest and wise payment. In 2026, personal loans will turn into one of the most flexible monetary tools for Americans dealing with increasing expenditures, financial obligation consolidation, emergency situations, and big life purchases.

Proven Strategies for Simplifying Credit Card Debt

Whether you are preparing a huge purchase, handling debt, or covering unexpected expenses, selecting the best personal loan in the U.S.A. can substantially impact your monetary health. However, with hundreds of lending institutions, different APR ranges, and hidden costs, selecting the ideal loan requires cautious understanding. This total guide will assist beginners, debtors, and finance readers comprehend how individual loans work in 2026 and how to discover the finest low-interest alternatives securely.

Unlike home mortgages or vehicle loans, personal loans generally do not require collateral. Key features of personal loans: Repaired interest rate (for the most part) Fixed regular monthly payments Versatile use (financial obligation, medical, travel, and so on) Loan terms typically between 1 to 7 years A lot of lending institutions in the U.S.A. deal personal loans ranging from about $1,000 to $50,000, though some institutions offer loans as much as $100,000 depending on eligibility.

Understanding rate of interest is the first action before requesting any loan. In 2026, individual loan APRs differ significantly based upon credit history, income, and lender policies. Current monetary data shows: Average personal loan rate around for borrowers with excellent credit Market APR range roughly depending on credit reliability Leading loan providers in early 2026 are using competitive starting APRs such as: Around 6.49% (LightStream) Around 6.74% (major banks) Around 6.99% (premium lenders) However, single-digit APRs are normally reserved for customers with excellent credit and strong monetary profiles.

Many borrowers prefer installment loans due to the fact that they provide clarity and control over repayment. Here are the main reasons Americans are picking personal loans in 2026: Personal loans typically have considerably lower interest rates than credit cards, making them perfect for financial obligation consolidation. Unlike revolving credit, individual loans have repaired EMIs (monthly payments), which helps in budgeting and monetary preparation.

Lots of online lenders in the U.S.A. now approve loans within 2448 hours, which is crucial for emergency situations. Not all personal loans are the very same. Comprehending various loan categories helps you pick the finest alternative based upon your financial objective. These loans are used to combine multiple debts into one regular monthly payment, typically at a lower rate of interest.

Navigating Debt-Relief Counseling for 2026

Online lenders normally supply faster funding for emergency situation loans. These loans are offered for borrowers with low credit ratings, though interest rates are typically higher.

This stability makes them much easier to manage compared to variable-rate credit alternatives. SoFi is among the most acknowledged digital lending institutions offering competitive APRs, versatile loan terms, and no surprise charges for certified customers. Why borrowers pick SoFi: Loan amounts approximately $100,000 Fixed rates Unemployment defense alternatives LightStream regularly ranks amongst top loan providers for customers with exceptional credit and provides some of the most affordable starting APRs in the market.

Normal features: Moderate APR variety credit union dependability flexible payment alternatives Upstart uses AI-based underwriting models and considers factors beyond simply credit rating, making it a strong alternative for younger borrowers and those with restricted credit history. Major banks still offer competitive individual loan products with APRs starting around the mid-single digits for qualified candidates.

How to Choose a Leading Nonprofit Financial Advisory

Normal rate expectations: Excellent credit (750+): Lowest APR (610%) Excellent credit (690749 ): Moderate APR (1015%) Fair credit (630689 ): Greater APR (1525%) Poor credit (

{kind=link}

Latest Posts

How to Find Lower Interest Private Loans

HUD-Approved Housing and Financial Education in 2026

Why Choose Nonprofit Debt Relief for 2026